Investment Strategy

A good investment strategy is not just about putting in place an efficient asset allocation for today. It should also incorporate how the strategy should change in the future, in order to best meet your objectives.

Each pension scheme faces its own specific set of issues. Each insurance activity has its own characteristics. Each fund has its own objectives. All this means that a "one size fits all" approach is rarely successful. We design and assist in implementing investment strategies specifically designed to meet your requirements and your objectives.

Setting up an investment strategy is the most important decision that trustees make. In doing so, they are required by legislation to consult with the sponsoring employer. Our advice is focused on helping our clients understand the risk and rewards of potential strategies to arrive at the right mix of asset classes for their scheme's circumstances.

Pension Fund Investment Strategy Roadmap

We use a straightforward roadmap which follows the following four questions:

| Strategy roadmap | |

| What do you want to achieve? | We start by helping you consider your objectives and those of other parties involved in the process. |

| Are you taking unnecessary risks? | By considering the risks being run by the scheme, you can determine which ones you are happy with and which ones you would rather reduce. |

| Are you putting all your eggs in one basket? | Once you have decided which risks to retain, we can help you decide how best to spread this risk between asset classes and managers. |

| How can your strategy be implemented intelligently? | Finally, the timing of the implementation of your chosen strategy can have a significant effect. We can help you to implement it in a sensible way, for example using switching mechanisms based on market levels. |

By navigating you through this roadmap, using appropriate and leading edge tools and clear communication, we will help you understand the "journey risk" - the risk of a significant deficit arising in the next few years, and the "destination risk" - the ultimate probability of meeting the benefit promise.

At the outset we educate clients about the nature of their scheme's future cash flows, and how the associated risks of meeting them can be managed. We will ensure that you understand your options and will give you a direct recommendation on the direction we think you should take.

Investment Strategy Roadmap in other activities

Setting up an investment strategy for insurance activities, mutual funds, other funds or other activities other than pension fund activities follows a similar logic. This means focusing on helping our clients understand the risk and rewards of potential strategies to arrive at the right mix of asset classes for their specific goals and objectives.

Each activity requires its own roadmap taking into account its specific situation.

Alternative asset classes

Alternative asset classes include:

- Diversified growth funds

- Commodities

- Infrastructure

- Active currency management

- Hedge funds

Diversifying into other asset classes like these can help make the investment strategy more efficient. It allows schemes to increase their expected returns for the same level of risk, or reduce risk without sacrificing expected returns.

We work with our clients to give them a much greater understanding of these unfamiliar assets. We provide an objective opinion of the benefits and drawbacks. This includes timely advice on relative attractiveness and appropriate levels of investment.

Liability Driven Investment

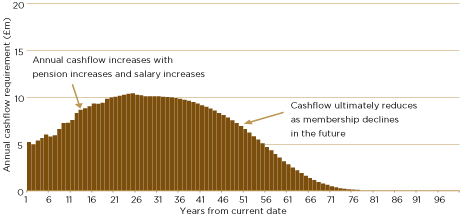

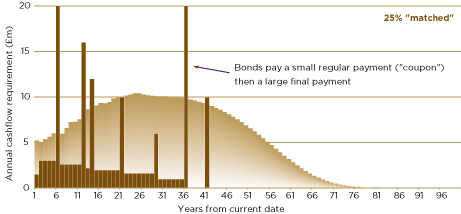

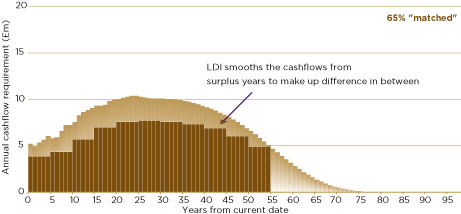

Liability Driven Investment ("LDI") is potentially useful in a range of circumstances. Its key attraction is that it has the potential to narrow the range of future investment outcomes. However, reducing the risk comes at a price: that of reducing potential returns. Using LDI makes assets and liabilities track each other more closely over time. It does this by matching the future cash coming from bonds with the future cash needed by the operation (pension scheme, insurance company or other) . It also reduces volatility. The following graphs show an example of liability driven investments for pension funds.

Scheme's expected cash flows (dark purple bars) show differing levels as membership falls.

Long dated government bonds show a mismatch between the scheme's cash flows (light purple line) and bond payouts (dark purple bars).

A well designed LDI solution should aim to be practical and to help match a scheme's cash flows, so that any investment solution and the expected cash flows move in tandem.